On January 16, 2025, the U.S. Division of Schooling introduced that federal scholar mortgage debtors can now, for the primary time, see what number of months of progress they’ve towards having any remaining steadiness on their loans cancelled via the Revenue-Pushed Reimbursement (IDR) plans. Debtors can see this info by logging in to their Federal Pupil Assist account at studentaid.gov. Debtors ought to contemplate taking screenshots or in any other case save information of their IDR qualifying cost counts in case this info is ever disputed or faraway from studentaid.gov.

Under, we cowl:

- What IDR qualifying funds counts and cost phrases are, and why they matter.

- How debtors can verify their IDR progress and save copies to guard their progress.

- How the one-time cost depend adjustment helped repair previous errors that prevented debtors from getting as a lot IDR qualifying credit score as they need to.

Revenue-Pushed Reimbursement (IDR) plans have been designed to supply debtors an inexpensive choice to repay their loans. IDR plans usually set month-to-month cost quantities primarily based on the borrower’s earnings and household dimension annually. Moreover, as a result of some debtors won’t make sufficient to totally repay their loans, even after paying for 20 years or extra, IDR plans provide a “mild on the finish of the tunnel” – a requirement that after a sure period of time in compensation, any remaining steadiness on the mortgage might be cancelled. The brand new software on studentaid.gov exhibits the borrower their IDR cost time period, what number of qualifying months of funds they’ve made, and what number of extra months of qualifying funds they have to make earlier than the excellent steadiness on their loans might be cancelled. Right here’s what every of those numbers imply.

Most IDR plans have a 20 or 25 12 months “cost time period,” which means that after 20 or 25 years of qualifying month-to-month funds (i.e., 240 or 300 month-to-month funds) any remaining steadiness on the mortgage might be cancelled. You’ll be able to be taught extra concerning the cost phrases of every of the IDR plans right here.

The SAVE plan, created by the Biden Administration in 2023, presents shorter cost phrases – between 10 and 19 years – for individuals who borrowed lower than $21,000 in federal scholar loans, together with most group faculty college students. Nonetheless, the SAVE plan is at the moment tied up within the courts following authorized challenges led by Missouri and Kansas, and Republicans members of Congress have just lately listed chopping the SAVE plan and elevating scholar mortgage funds as a possible option to pay for proposed tax legal guidelines.

“Qualifying funds” imply month-to-month funds, or sure different compensation statuses, that depend towards reaching the tip of the IDR cost time period and qualifying to have any remaining steadiness cancelled. Months with the next funds or statuses are thought-about qualifying funds:

- full, on-time funds in any of the IDR plans (together with the SAVE plan, REPAYE plan, PAYE plan, IBR plan, and ICR plan), together with months the place the borrower owed $0 of their IDR plan

- full, on-time funds in a 10-year Commonplace plan,

- all time within the COVID-19 Cost Pause,

- time in some forms of deferments or forbearances or deferments

IDR qualifying cost counts present the variety of months of qualifying funds the borrower has already made towards the whole variety of qualifying months required for cancellation via the IDR program. Equally, the time till the finish of the IDR cost time period exhibits what number of extra years and months of qualifying funds the borrower should make till they qualify to have any remaining steadiness cancelled.

Instance: Ava is enrolled within the PAYE plan and has a 20-year IDR cost time period, which means any remaining mortgage steadiness might be cancelled after she makes a complete of 240 qualifying month-to-month funds. Ava has been making qualifying funds on her loans since January 2013 and now has an IDR qualifying cost depend of 144 (12 years of 12 month-to-month funds). Ava has to make 8 extra years of qualifying funds (96 extra qualifying funds) till she reaches the finish of her IDR cost time period and any remaining steadiness is canceled.

Importantly, some debtors will repay their loans earlier than the tip of their IDR cost time period. As a result of IDR funds are set primarily based on earnings moderately than on the mortgage quantity, some debtors find yourself absolutely repaying their loans in IDR plans earlier than the tip of the IDR cost time period. As soon as the borrower has repaid their mortgage steadiness in full, the mortgage is paid off and they don’t have to make any extra funds, even when there may be extra time left of their IDR cost time period. Moreover, debtors who work in public service could also be eligible for mortgage cancellation after 10 years of qualifying funds via the Public Service Mortgage Forgiveness (PSLF) program.

To verify your progress towards reaching the tip of your IDR cost time period and having any remaining steadiness in your mortgage cancelled, take the next steps:

- Log into your federal scholar help account on studentaid.gov.

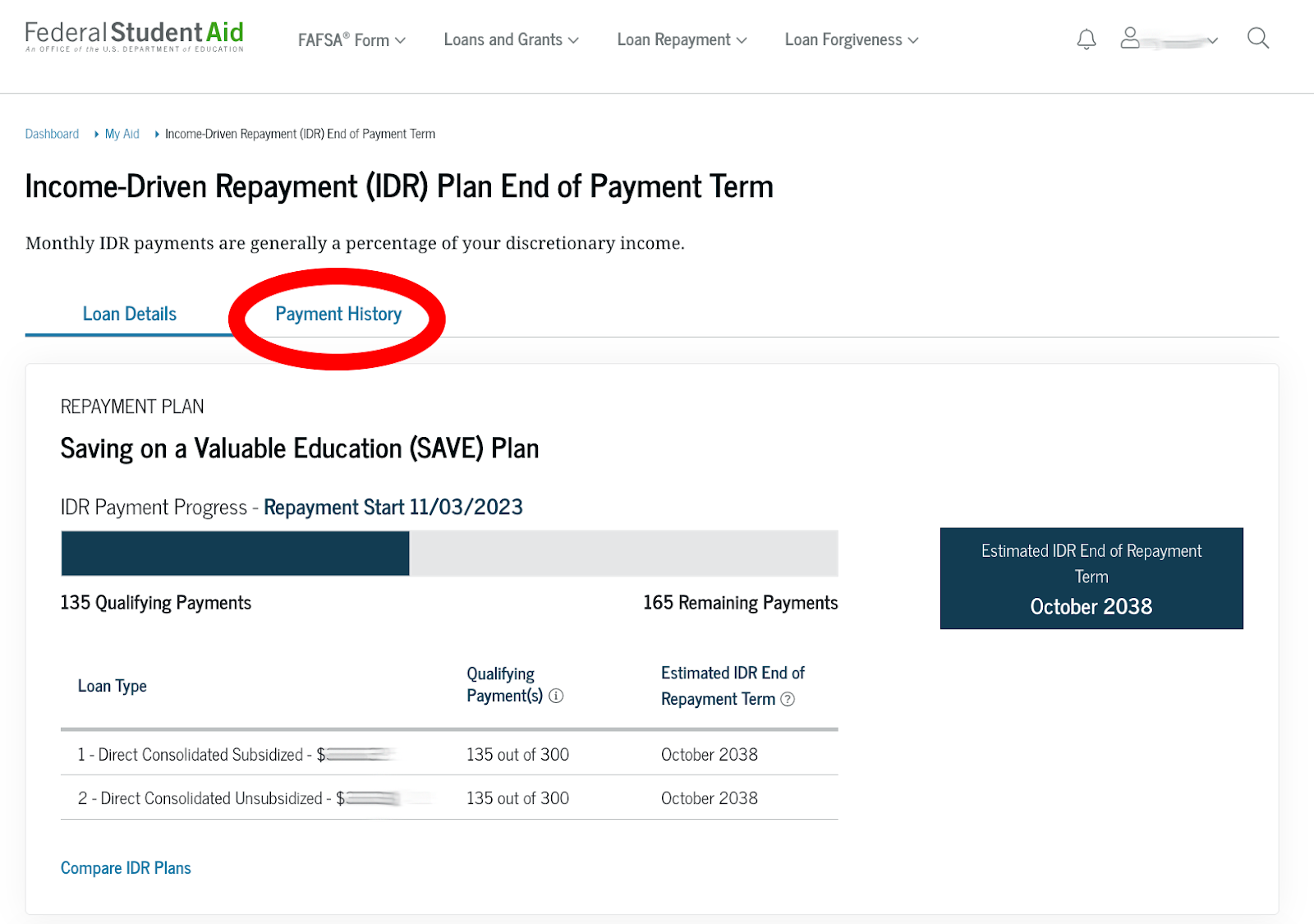

- You must now see your “scholar help dashboard.” On the appropriate hand aspect of the display, there’s a new part displaying you ways a lot time is left till the Finish of IDR Cost Time period. That is what number of extra years and months of qualifying funds you will want to make earlier than you qualify to have any remaining steadiness in your scholar loans canceled. Under is an instance of what you’re searching for in your dashboard:

- Contemplate taking a screenshot and saving it to your information, or printing the web page to PDF and saving it to your information. This might be helpful if the Division of Schooling stops presenting or updating this info on studentaid.gov, or if in case you have a dispute along with your servicer or the Division about your qualifying time towards mortgage cancellation.

- Subsequent, click on on “View IDR Progress,” which is able to take you to a web page the place you’ll be able to see your qualifying cost depend for every of your federal scholar loans. Beneath “Qualifying Cost(s)” you will note, for every of your loans, what number of qualifying funds you will have already made towards qualifying to have the remaining steadiness of your mortgage cancelled through IDR. Once more, contemplate saving screenshots, or printing to PDF and saving to your information. An instance is under:

{kind=link}

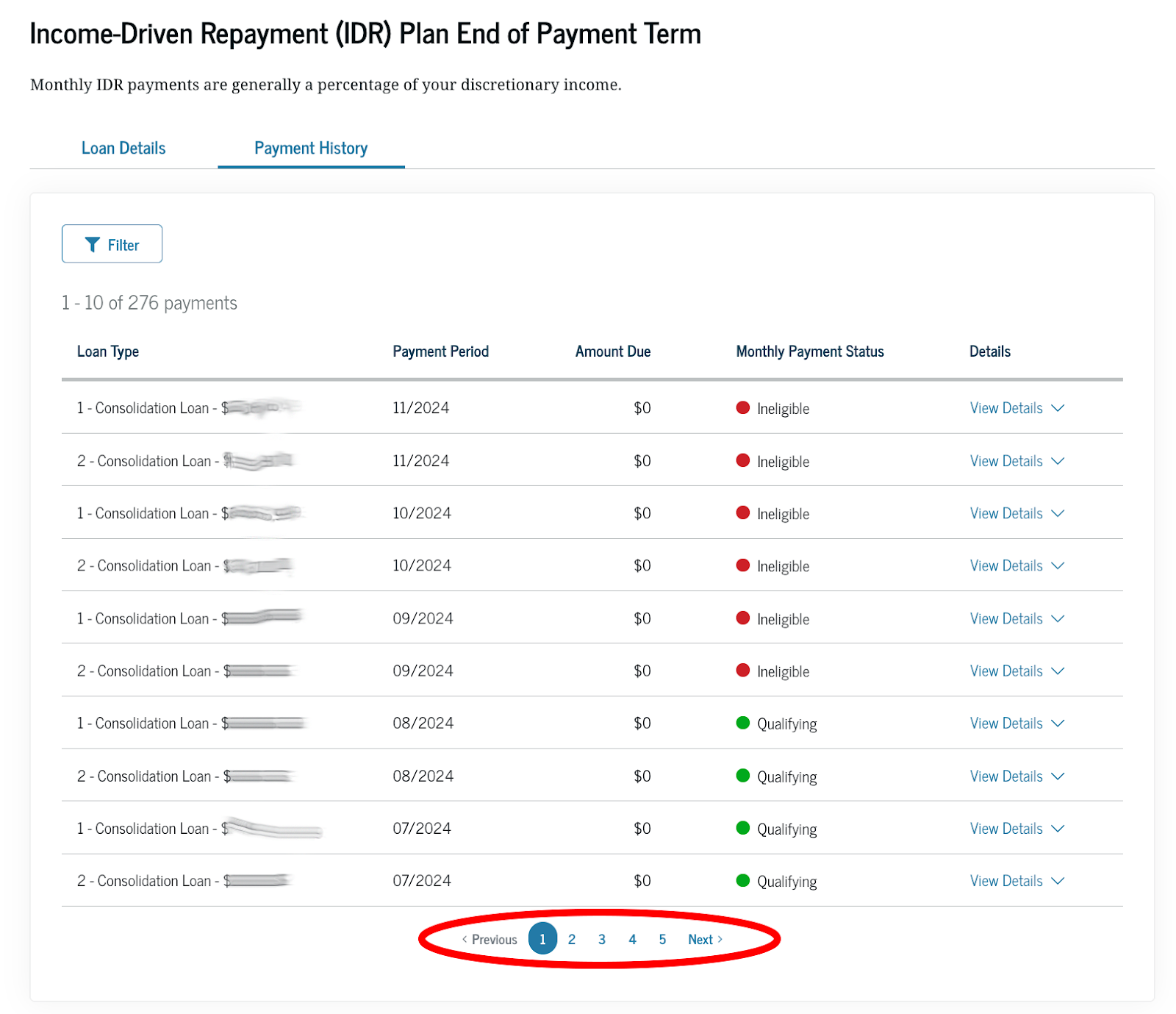

- Subsequent, click on “Cost Historical past.” This web page will present you for each month because you began repaying every of your loans, whether or not the Division has recorded that month as a “qualifying” cost month towards your IDR cost time period, vs “ineligible.” An instance is under. In case you click on on the filter, below “Cost Standing” you’ll be able to choose not qualifying to see all the months which have been marked ineligible on every mortgage. Search for any months marked as “ineligible” that you just assume is perhaps a mistake. In case you discover any errors, contemplate submitting a criticism and request for correction with the FSA Ombudsman. And once more, contemplate saving screenshots or PDFs of the total cost historical past for every of your loans in your information. Solely ten entries present at a time, so ensure you take an image of every web page of eligible and ineligible funds.

The newly seen IDR cost counts mirror changes made below the one-time cost depend adjustment (also referred to as the “IDR Account Adjustment”) first introduced in 2022. For a lot of debtors, these changes elevated their qualifying cost depend by correcting for previous servicing and record-keeping errors that prevented debtors from getting as a lot qualifying time towards reaching IDR cancellation as they’d have if the system was working.

The one-time cost depend adjustment was accomplished in phases, and has already helped the 1.45 million debtors who certified to have their loans cancelled via IDR plans over the past 4 years. Beforehand, solely 50 (!) debtors had their loans cancelled via IDR plans.

The Division of Schooling introduced on January 16, 2025, that it had largely accomplished the one-time cost depend adjustment, and that the qualifying cost counts now viewable on studentaid.gov mirror the changes to debtors’ accounts.

For extra details about the one-time cost depend adjustment, see right here.